G20 game over? Three reasons why the Finance Ministers’ meeting shows the G20’s time may be up

The G20 Finance Ministers of the world’s largest economies met in Buenos Aires last weekend, but their failure to tackle pressing global problems, including the threat of trade wars and a looming debt crisis, highlighted how ineffective the G20 has become. Given that the G20 cannot tackle key issues, is promoting ineffective initiatives, and has largely become a rubber stamping body for other actors, the time is ripe to rethink how the global economy is governed, and to promote alternatives.

1. The G20 cannot tackle key issues

The 2017 G20 showed how the ‘anti-multilateralism’ approach of the world’s major powers immediately dampened the prospects of new initiatives coming out of the G20, as Eurodad reported at the time. It is no surprise, therefore, that despite the threat of global trade wars being among the hottest topics that finance ministers ought to be tackling, trade gets only a passing mention in the communiqué.

More surprising however, is the G20’s lacklustre approach to the growing global problem of debt. As the IMF highlighted earlier this year, forty per cent of low-income developing countries are now at high risk of, or in, debt distress. While the G20 Finance Ministers “continue to monitor debt vulnerabilities in Low Income Countries (LICs) with concern” the only solutions they offer put the burden onto those countries: “building capacity in public financial management, strengthening domestic policy frameworks, and enhancing information sharing”.

Perhaps more shocking is the communiqué’s failure to acknowledge that debt is not just a low-income country problem. While high-income countries such as Greece continue to struggle under creditor-imposed austerity in response to debt crisis, middle-income and emerging market countries are also facing major problems. In fact, all developing countries are suffering from the impacts of monetary policy changes in rich countries. Argentina, for example, has seen investors pulling out and its currency plummet and was forced to agree a $50 billion loan from the IMF earlier this year – its largest ever loan - with, sadly, the usual damaging austerity policies attached.

As Eurodad previously noted, the G20 continues to ignore the strong work that UN institutions have undertaken in this area, including developing principles for responsible lending and borrowing, and the adoption by the UN General Assembly of Basic Principles for Sovereign Debt Restructuring in 2015. The lack of a fair, transparent and rapid Debt Resolution Forum to help countries in debt crises continues to be a major gap in the international economic architecture, and one that the G20 looks incapable of even recognising, let alone filling.

2. Existing G20 initiatives are proving ineffective

Tax is one key area where the G20 initiated reforms for many years, and which became a major G20 priority in 2013. Sadly, however, the communiqué confirms how ineffective their approach has been.

The communiqué highlights “the importance of the worldwide implementation of the Base Erosion and Profit Shifting (BEPS) package.” Eurodad has already noted the major flaws of BEPS, an OECD initiative: it lacks transparency, contains significant loopholes, and favours OECD countries over developing countries, which have had little meaningful participation in decision-making.

Unfortunately, the G20 appears to double down on this flawed OECD-led approach, by promising to “address the impacts of the digitalisation of the economy on the international tax system by 2020,” but including as their only background paper a statement from the OECD Secretary General on the issue. This means, once again, that international tax standards are likely to be developed in a highly opaque forum where tax havens are heavily over-represented, but a large proportion of developing countries are excluded.

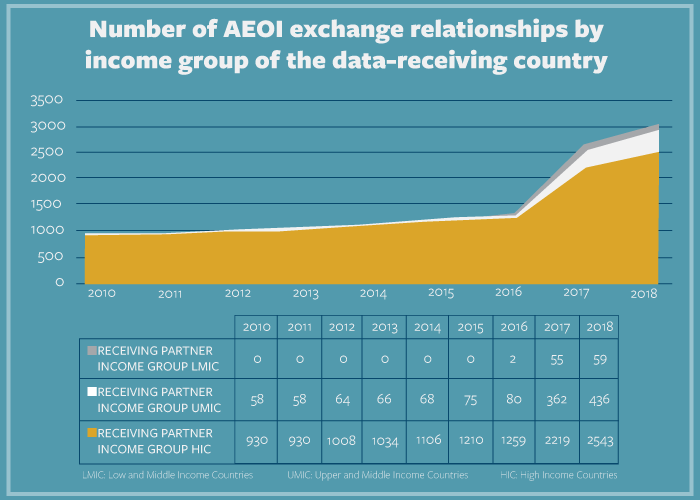

The G20 Finance Ministers also “support the OECD strengthened criteria to identify jurisdictions that have not satisfactorily implemented the internationally agreed tax transparency standards.” However, these standards are deeply flawed for two main reasons. Firstly, they don’t oblige countries to share information with all other signatories, relying instead on a "dating game" approach, where governments can decide to share information with some countries but not others. This is an important reason why the world's poorest countries are currently receiving much less information than richer countries, as illustrated in this infographic.

{kind=link}

Secondly, the standards remain overly cumbersome for least developed countries. For example, despite strong campaigning from civil society organisations, the OECD and G20 rejected a proposal to introduce a transitional ‘non-reciprocity’ period, where countries with low levels of resources can receive information, even if they are not able to send information back.

The bottom line is that we still do not have the ambitious international standards needed to tackle international tax avoidance and evasion, and thereby mobilise additional financing for development. One important reason for this is the OECD and G20’s problematic tradition of negotiating tax and transparency standards in closed confidential negotiations where the world’s tax havens are well represented, while a large part of the world’s poorest countries are excluded. The obvious and much better alternative would be to move international tax discussions to the United Nations, as called for by Eurodad and others.

3. Is the G20 really in the driving seat?

In many ways, the G20 has become a rubber-stamping institution for initiatives dreamed up by other actors. The issue of infrastructure – an Argentinian G20 priority – is a case in point. One key G20 focus has been the development of an “asset class” for infrastructure, for which it is currently developing a “Roadmap”. Transforming infrastructure into a tradable asset class would mean repackaging money invested in an infrastructure project into a number of standardised financial instruments which are easy to buy and sell, and which provide an attractive revenue stream for institutional investors, such as pension and insurance funds. This is an idea that has been heavily promoted by the World Bank Group and OECD, which wrote the G20 Finance Ministers’ background document on the issue.

As a recent Civil20 policy paper has pointed out, however, there are three many reasons why this is a bad idea. Firstly, it ignores the main issue: how to increase and improve the quality of public investment. Historically, infrastructure projects in developing countries have been overwhelmingly financed through public investment, 80-85 per cent according to World Bank research and virtually 100 per cent in some fast growing economies, including China. Secondly, it is likely to prove very costly for the public purse as investors will require strong public subsidies and guarantees in order to transform long-term and risky infrastructure investments, many with low commercial potential, into tradable assets offering attractive returns. Thirdly, an infrastructure asset class would be a massive leap in the dark into uncharted territory – a 2018 World Bank report reveals that “…the [current] contribution of institutional investors is miniscule, at only 0.67 per cent of the total global [private participation in infrastructure]”.

In order to promote this mistaken agenda, G20 Finance Ministers also pushed for progress in areas such as “risk mitigation and credit enhancements, data availability, and contractual and financial standardisation.” While standard contracts for infrastructure projects may be good for the private sector, they could threaten infrastructure quality by reducing essential public oversight and weakening environmental and social standards. For instance, the World Bank’s attempts to standardise public-private partnership (PPP) contracts have, according to a recent legal analysis, resulted in proposals that favour the interests of the private investors over public partners.

It may not be the World Bank and OECD that are really behind this agenda, however. According to the World Economic Forum (WEF), institutional investors, holding trillions of dollars under management, and seeking a diversified portfolio of infrastructure assets with attractive returns, have exerted pressure to launch several infrastructure funds. The G20 is also now getting advice from an infrastructure ‘Private Sector Advisory Group’, which was convened in March to move forward the G20’s infrastructure agenda. Though this group is shrouded in secrecy – with no participants list or terms of reference currently available – indications suggests that it contains several financial sector actors who would be major beneficiaries of the creation of a new asset class for infrastructure.

What’s the alternative?

These three failings are all linked to how the G20 is structured. As an informal club that operates by consensus, its ability to reach agreement can be held to ransom by powerful countries, such as the US, refusing to cooperate. As it excludes the vast majority of countries from having any meaningful input, and relies on bodies such as the OECD which also exclude most developing countries, it is prone to adopting ineffective solutions. As it has no permanent secretariat, the scope and impact of its agenda shifts annually depending on who is hosting, and the only follow-up can be through existing institutions, which use the G20 to push their own agendas. As there is no mechanism for countries to join the G20, it will inevitably become out of date, so will not even represent the largest economies in the world.

One elegant solution is to replace the G20 with an economic coordination council elected by all UN member states, as proposed by the UN Commission of Experts on reforms of the international monetary and financial system. This would allow all countries a means of input, while also keeping the body small enough to make practical decisions. By being embedded in the UN, it would also provide the means to enforce and follow up on decisions. Such a council will not arrive overnight, of course, but it is time for those who are serious about tackling global problems to begin to advocate for alternatives to the failing G20 model.